Altisource Portfolio Solutions $ASPS

Altisource Portfolio Solutions $ASPS

Contrarian, Countercyclical. Betting on a return to profitability. Commentary + Buyside Research from SA

Disclaimer: Do you own investment research, this newsletter is for entertainment and informational purposes only. The author is not responsible for any losses incurred. What you are reading is not investment advice. The stocks mentioned in this post are not investment recommendations.

Altisource Portfolio Solutions is a Luxembourg based integrated service provider and marketplace for the real estate and mortgage industry in the United States and internationally. It provides foreclosure, short sale, and eviction management services. The company provides title insurance, risk mitigation, appraisal, inspection, trustee, and loan technology services to a variety of bank, non bank, and government customers.

Altisource runs a business-to-business company primarily focused on providing technology and related services to lenders. This involves appraisal, auction, inspection, etc. The company was a beneficiary of the 2008-2011 Housing Crisis where a flood of demand for foreclosure, short sale, and eviction related services propelled Altisource from under $6 a share to over $160 a share in 2013. Since 2013, the company has shown consistently declining revenues as the number of foreclosure and distressed property services utilized by lenders has steadily declined.

In short, $ASPS may be a potential counter-cyclical speculative play on the eventual lifting of foreclosure and eviction moratoriums. During 2020, Altisource’s revenue and earnings-per-share fell dramatically as the extended federal, state, and local foreclosure and eviction moratoriums essentially halted business. With a potential turn in the foreclosure cycle imminent, Altisource is poised to potentially return to profitability in the next 18-24 months. The tremendous backlog in lender demand for mortgage delinquency related services could eventually lift Altisource’s revenue and drive speculators back into Altisource’s low-volume, small cap stock.

Altisource has lost several key customers last year and faces increased competition in its declining market niche. Altisource’s cashflows have a high correlation to the foreclosure cycle. After foreclosure and eviction moratoriums are lifted, Altisource could see a dramatic rise in revenue within 12-18 months, a return to profitability, and some renewed optimism around the beaten down stock.

A risk is that foreclosure moratoriums are extended into mid-2022 or beyond under a blue government while the company continues to burn cash. A further risk is that since Altisource’s stock ($ASPS) has a market capitalization of only 146 million dollars, (making it small cap) a decline in this high beta stock could get $ASPS delisted into microcap territory causing institutional selling. $ASPS has been acting like a rollercoaster over the last 12 months due to multiple earnings misses, analyst downgrades, and moratorium extensions. Speculators need to be able to either stomach this volatility or buy puts on $ASPS for hedging.

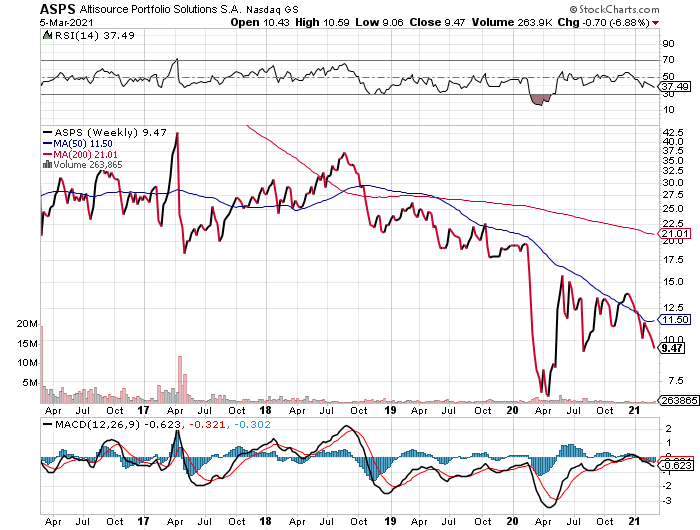

With the stock crossing below the blue-line above (50-day Moving Average) in January along with a technical “death-cross” of the 50-day MA crossing below the 200 day MA in July of 2020; the stock has had abysmal performance aided by abysmal fundamentals. Due to the complicated nature of state, local, county, CDC, and federal eviction and foreclosure moratoriums, speculators in $ASPS stock should focus on the headline federal policy for properties with FHA or other federal financing. If federal moratoriums are extended past June and into 2022 or beyond, $ASPS is likely to retest the April lows of $7 a share as Mr. Market sells the news of a moratorium extension.

$ASPS could be a decent longer-term speculation or a portfolio hedge around an eventual rise in demand for mortgage delinquency services with potential multi-bagger upside, however this stock comes with serious volatility, market cap, and political risk.

Below is buy-side research from Seekingalpha.com:

https://seekingalpha.com/article/4317594-altisource-stay-patient-cycle-turn-not-imminent

https://seekingalpha.com/article/4357120-too-early-to-buy-altisource-portfolio-solutions (Copied Below)

Too Early To Buy Altisource Portfolio Solutions

Jul. 06, 2020 11:53 AM ET Altisource Portfolio Solutions S.A. (ASPS)

Summary

Altisource is an asset-light, counter-cyclical business model.

The CARES Act will delay foreclosures until 2021, meaning that financial results in 2020 should be down by 40%.

Wait until Q4 to see signs of an inflection point. Once the default cycle turns, ASPS could be a multi-bagger.

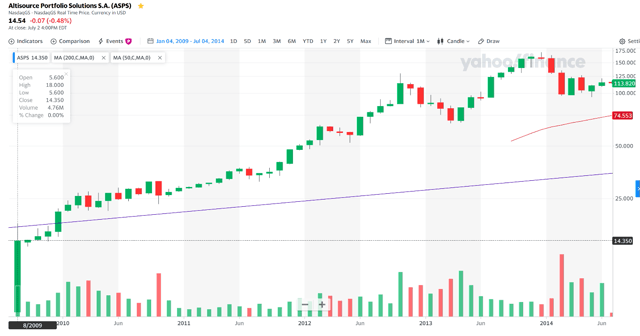

One of the big winners of the mortgage crisis of 2008 was Altisource Portfolio Solutions (NASDAQ:ASPS). The stock rose from $5.60 to over $150 share in less than five years as mortgage delinquencies skyrocketed. Due to the pandemic, mortgage delinquencies are on the rise again. However, the Coronavirus Aid, Relief, and Economic Security (CARES) Act has put a halt to foreclosures. Subsequently, Altisource has yet to see an uptick in its business, and the inflection point will most likely be in Q1 of next year.

Source: Yahoo Finance

Mortgage Delinquencies On the Rise

In May, it was reported that the number of borrowers more than 30 days late swelled to 4.3 million, up 723,000 from the previous month. More than 8% of all U.S. mortgages were past due or in foreclosure.

Source: Bloomberg

Source: Black Knight

The current surge in delinquencies is even greater than 2009. The five-year period where mortgage delinquencies rose from 1.5% to 5% resulted in a 30X move in the stock price of ASPS. The question is whether this is the beginning of a multi-year cycle for whether the economy will quickly regain its footing in the second half of 2020.

Thus far, ASPS has not seen any benefit from the rise in mortgage delinquencies due to the CARES Act. At the height of the pandemic, a temporary halt to foreclosures until August 31, 2020, was enacted. In addition, mortgagees have the option to apply for loan forbearance if they experienced financial hardship due to the pandemic. The loan forbearance can be up to 360 days in length.

No Uptick Until Next Year

On the most recent conference call, CEO Bill Shepro noted that there would not be an uptick in business until maybe Q1 of next year.

"So what we anticipate is going to happen, is that, as these moratoriums come to an end, we will see a pickup of referrals both foreclosure-related referral, scenario related referrals. But in terms of a large increase from where we might have otherwise have been this year, I don't think we'll start seeing that impact until you get into maybe the fourth quarter and into the first quarter of next year, when those forbearance period start to expire." - Source: ASPS Q1 2020 Earnings Conference Call

It should also be noted that it takes time for a default to be passed along to ASPS for processing. After the mortgage is in default for 15 days, ASPS sends the first mailing. However, it can take 180 days after a foreclosure for the company to book any revenue from the operation. Thus, there is a long lag time that is further complicated by the CARES Act.

Valuation

ASPS has a market cap of $227 million and an enterprise value of $422 million.

I am currently modeling a 40% decline in revenues for 2020. This would result in revenues of $360 million. The company will most likely lose almost $1/share in 2020.

The balance sheet is far from pristine. The company has $304 million of debt. Operating cash flow was negative $1.6 million in Q1. With $120 million of cash, ASPS should be able to weather a difficult 2020.

Up Cycle in 2021?

If you believe that mortgage delinquency has started a multi-year cycle, ASPS could be a big winner. With a small uptick in mortgage delinquencies, the company could earn $100 million of cash flow in 2021. If you put a 10X P/CF multiple, you come up with a stock that could quadruple. However, ASPS is a company that you want to revisit later in the year to see some signs that the business is at an inflection point. To put things into perspective, the company earned over $1 billion in CF during the 2009 crisis. The upside is enormous for a company with only a $227 million market cap.

The prudent move is to wait for signs of inflection before buying shares of ASPS. Despite the fact that mortgage delinquencies are surging, it will take several months for ASPS to see an uptick in the business.

Second article (too long to fit in the post): https://seekingalpha.com/article/4317594-altisource-stay-patient-cycle-turn-not-imminent