Housing Continues to Outperform

Housing Continues to Outperform

Year-end Forecast.

Disclaimer: Do you own investment research, this newsletter is for entertainment and informational purposes only. The author is not responsible for any losses incurred. What you are reading is not investment advice.

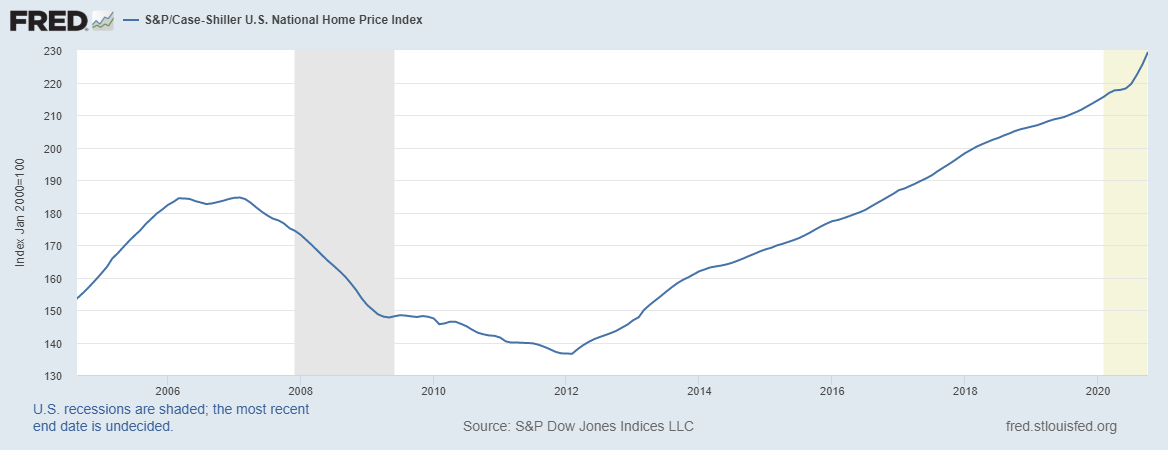

On Tuesday, the S&P CoreLogic Case-Shiller National Home Price Index was released for the month of October. The twenty city index beat analyst expectations showing a 8.4% gain in October ‘20 median home prices compared with October ‘19, up from 7% growth in September.

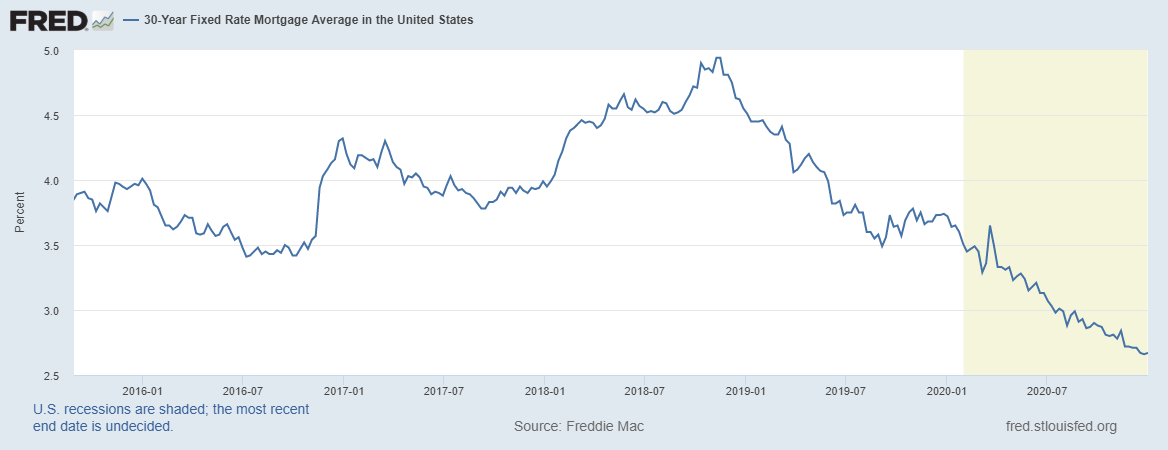

30 year fixed mortgage rates will end 2020 at an all time low of ~2.7%.

Every one-hundred basis point drop in interest rates typically corresponds to a 10% increase in home prices. Lower interest rates give buyers more purchasing power. Mortgage rates have moved from ~3.5% to ~2.7% in one year as the gap between the 10yr Treasury and 30yr Mortgage Rate closes. The 10yr yield has been moving higher for the past few months on vaccine and economic recovery hopes, however the correlation between the 10yr and mortgage rates has changed as the Federal Reserve fearing higher interest rates has purchased billions in Mortgage Backed Securities (MBS) to prevent mortgage rates from normalizing. If the Fed continues buying MBS, mortgage rates will remain pinned below 3% next year. Rising inflation expectations stemming from the ballooning of the Federal Reserve’s balance sheet and monetization of huge national deficits could spark a sell-off in the bond market, pushing yields higher, this is unlikely in the short-term, so the low interest rate tailwind likely remains in 2021.

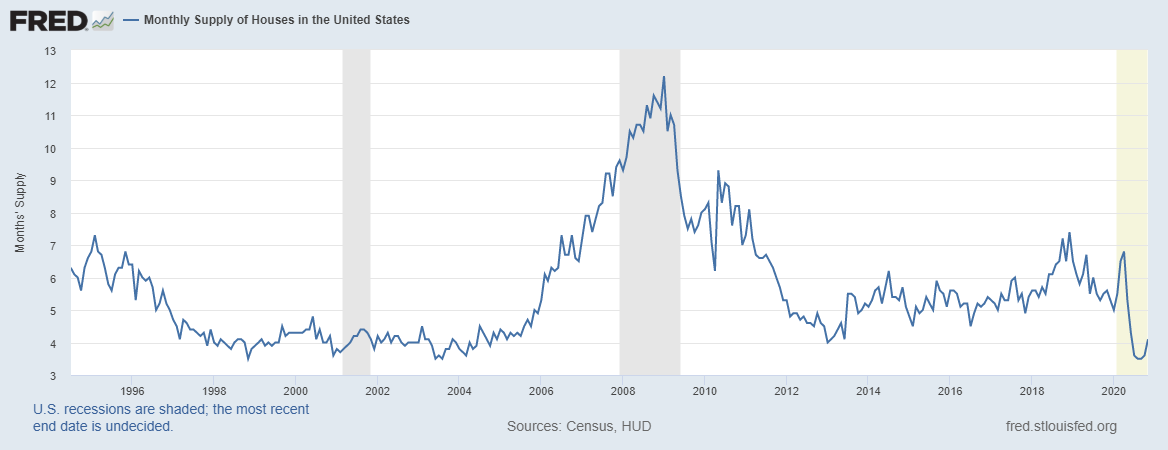

Supply is the next factor affecting home prices. Housing supply is at an all time low. As builders were traumatized by the 2008 housing crash, new supply came into the market too little too late. Additionally, sellers are reluctant to list their homes in the middle of a pandemic. Combine this trend with the strong demand-side effects of low interest rates and the mass exodus from urban centers into suburban single family homes and a short-term melt-up of home prices emerges as days on market fall and bidding wars increase.

Supply is likely to increase in 2021 as the housing market somewhat normalizes with pent up supply coming on the market (foreclosure moratorium lifted, Covid-19 holdouts). The question of how much will housing supply increase in the next 12-18 months holds the key to price action. Giving the bulls the benefit of the doubt, lets say interest rates stay at these artificial lows. The demand-side effect of low rates can be compared to a sugar-high for the housing market, it eventually wears off. If real estate values become tied to artificially low interest rates like they are in Europe, any future rate increases would spell trouble for housing (this happened in the U.S. in Q4 2018 as mortgage rates went up to ~5% and prices began to fall, before the Fed quickly reversed policy).

Assuming the bulls are right and additional demand for single family homes from the urban exodus continues indefinitely and doesn’t run out, the market still has to deal with pent-up supply. Some estimates say that more than a million homes are already in late stage default and several million others are in forbearance programs. If forbearance and foreclosure moratoriums end sometime next year, a wave of distressed properties could create “supply.” This “wave” of distressed properties hitting the market is a common pattern during recessions in 1990, 2008, and the early 1980s. FHA loans in some areas have delinquency rates of up to 15%. If the Biden administration decides to aid at risk borrowers, new “supply” will be avoided or delayed and forbearance programs will likely continue.

Future stagflation is a risk. Higher inflation as a result of the Fed’s monetization of record debt could cause interest rates to spike substantially in the future (speculation). Higher interest rates combined with a weak economy would be an ideal set up for the next bear market in housing. With inflation adjusted median home prices in many metros higher than their 2006 bubble highs, valuations in some places are historically high relative to wages and pose a significant threat to future returns.

")

The orange line represents inflation-adjusted home prices. The chart only goes up to July 2019. Both lines are higher today.

Because of historically high valuations (PE Ratio/Cap Rates), high defaults, lack of affordability, and the prospectus of pent-up supply, weaker demand next year, and/or higher interest rates in a stagflationary macro environment, the investment outlook for residential real estate in the next 18-24 months remains cautious hold. Housing very well could continue to rally if interest rates are further manipulated lower by dovish Fed policy. Continued forbearance, urban exodus, and the formation of millennial households are major tailwinds for housing. There is a limit to how high housing prices can rally, absent hyperinflation. As prices grow more and more out of step with wages, a correction becomes more likely. Housing has become increasingly “financialized,” becoming more and more correlated to the stock market and broader risk assets. The U.S. Economy is based on three things: debt, consumption, and asset prices. If one of these dominos falls it’s game over. Housing remains a historically prudent investment, however alike stocks, high valuations lead to lower prospective future returns. Typically the craziest part of financial manias or bubbles is at the end, this crazy Pandemic melt-up in asset prices could be no different. However, high valuations are no precursor to a bust. Just as you think something is overvalued it becomes overvalued squared.

Investors need to realize that smart investing is a “compared to what” game. How does 10% sound? Well what about the risks? Compared to what? The purpose of this post is less about trying to call a top in a generally overvalued asset class, but to get the idea of “compared to what?” across. It never is different, not this time, not ever, human psychology will create excesses and opportunities in financial markets for the rest of time. As value investors we have to stick to our principles and only buy cheap. The more quantitatively overvalued risk assets like housing become, the less attractive they are in the “compared to what?” game. Investors don’t have to reinvent the wheel; learn from the great value investors of the past like Walter Schloss, Warren Buffet, and Benjamin Graham. I wish everyone a prosperous new year!

Thanks, Kevin Habek